The retail lending boom in tier-2, tier-3, and rural India has been built on the back of the New-to-Credit (NTC) borrower. Driven by data-backed fintechs and digital NBFCs, millions of individuals are accessing formal credit for the very first time in their lives.

This access presents a massive growth opportunity, but it comes with an operational catch.

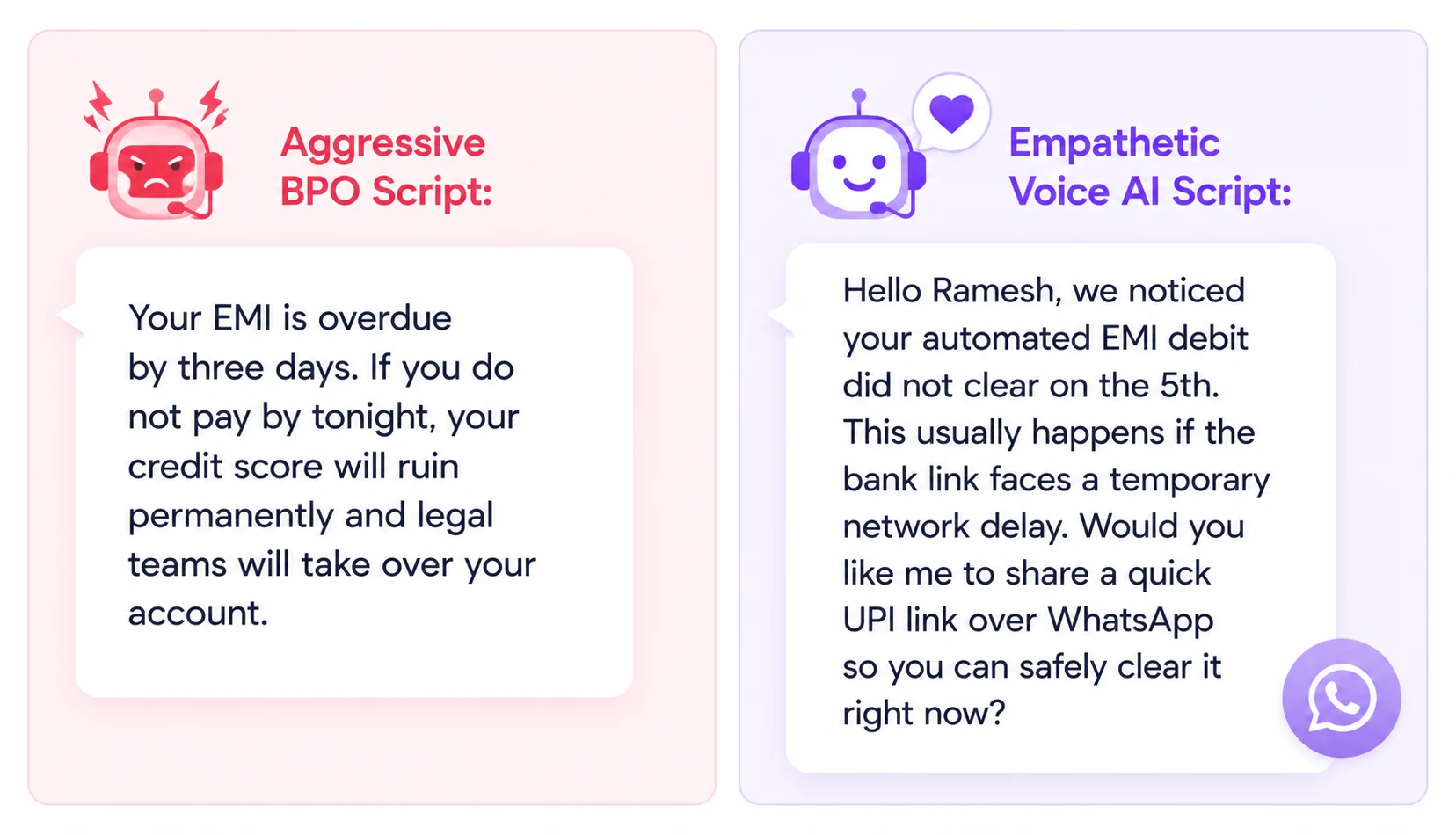

NTC borrowers frequently default on their first or second Equated Monthly Installment (EMI). However, unlike chronic defaulters who intentionally avoid payment, an NTC borrower usually misses a payment due to logistical confusion. They might not understand how an automated National Automated Clearing House (NACH) debit mandate works, they might fail to fund their bank account on the exact correct date, or they might simply be confused by a digital payment interface.

When a lender hands these fragile, early-stage collections over to traditional third-party recovery BPOs, the results are often disastrous.

Aggressive dunning scripts, intense caller pressure, and rigid language constraints alienate borrowers who simply needed guidance. The borrower pays the single overdue bill out of fear, but they never take another loan from that platform again. Your lifetime customer value plummets.

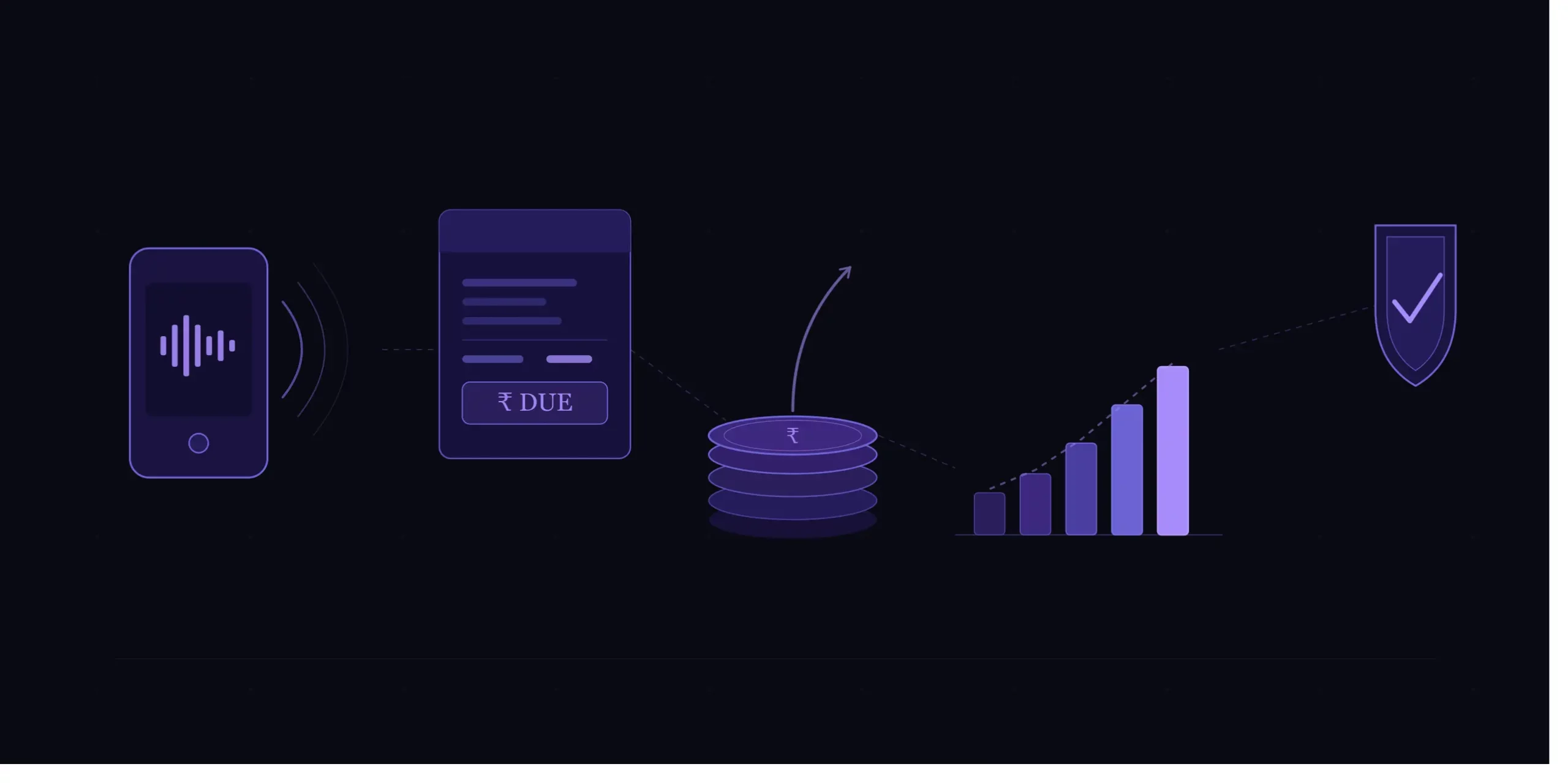

This is where a dedicated AI voice agent for EMI collection redefines the mechanics of early-stage financial recovery.

This structural shift transforms a high-pressure demand into a helpful service reminder, keeping your brand perception positive while ensuring the debt gets cleared.

This structural shift transforms a high-pressure demand into a helpful service reminder, keeping your brand perception positive while ensuring the debt gets cleared.