Voice AI: Voice AI is an artificial intelligence system that enables machines to understand, process, and respond to human speech in natural language through real-time voice conversations.

ASR (Automatic Speech Recognition): Technology that converts spoken audio into text in real time. In loan inquiry calls, ASR transcribes the borrower’s question so the system can process it instantly.

NLU (Natural Language Understanding): A layer of AI that identifies the caller’s intent (e.g., “loan status”) and extracts key details like loan ID, name, or date from the transcribed speech.

Voice Biometric Authentication: A security method that verifies a caller’s identity by matching their voice to a stored voiceprint. Used to reduce manual KYC time during loan status calls.

LOS (Loan Origination System): The core banking system that manages loan applications, approval stages, document tracking, and disbursal workflows. Voice AI connects to the LOS via APIs to fetch real-time status updates.

CRM (Customer Relationship Management): A system that stores customer records, interaction history, and contact details. It helps match incoming calls to the correct loan application.

API (Application Programming Interface): A secure digital bridge that allows Voice AI to request and retrieve data (like application status) from backend systems such as LOS or CRM.

FCR (First Call Resolution): The percentage of customer queries resolved in a single interaction without escalation or repeat calls.

AHT (Average Handle Time): The total time taken to complete a call, including verification, processing, and response delivery.

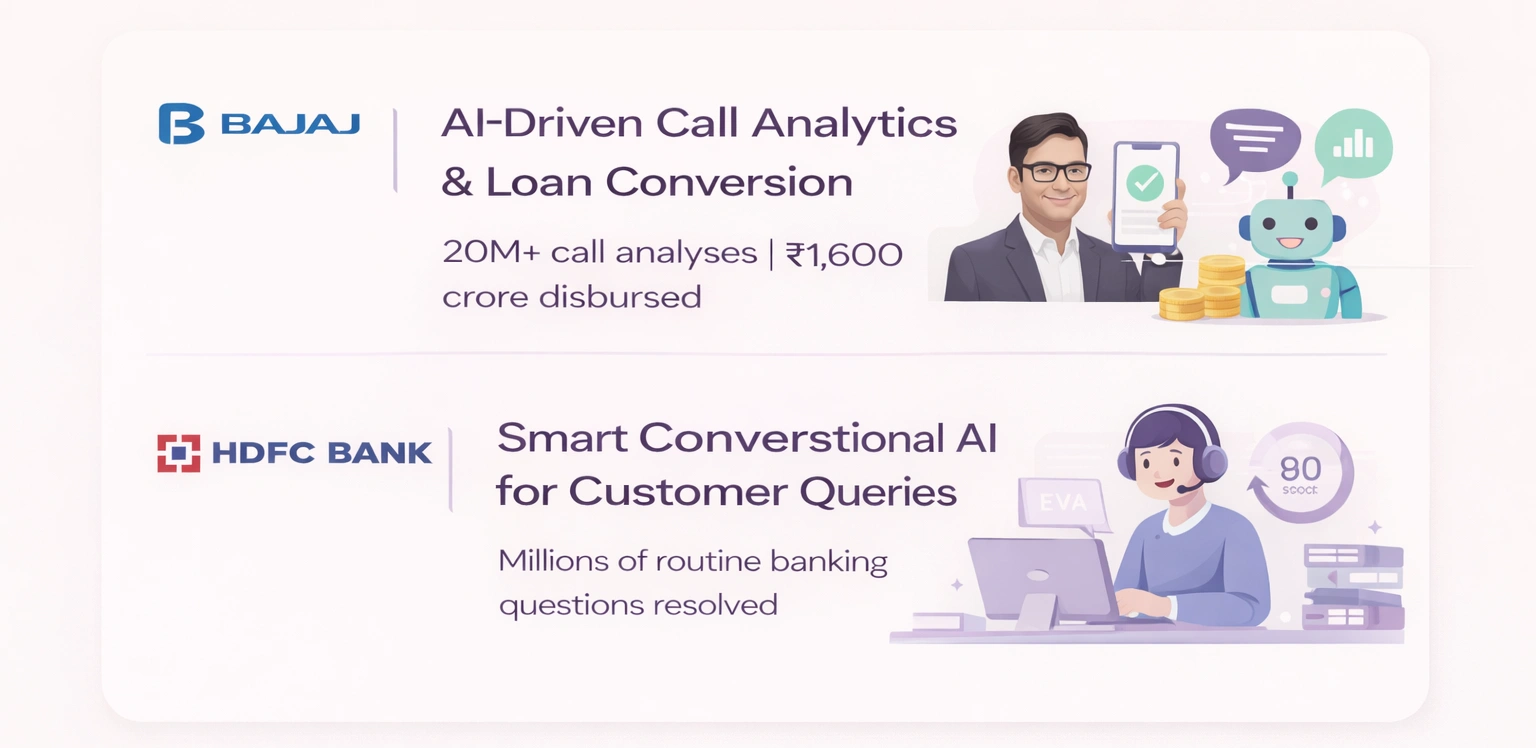

Let’s move from theory to receipts. Here are what actual Indian financial institutions are doing with Voice AI, with real numbers where available.

Let’s move from theory to receipts. Here are what actual Indian financial institutions are doing with Voice AI, with real numbers where available.